Calculating your MTD qualifying income the wrong way could put you in — or out — of scope. HMRC does not flag the mistake in advance.

MTD qualifying income is a specific figure defined by HMRC. It is not the same as your profit, your take-home pay, or your total household income.

Getting this wrong can be more costly than it looks. You could prepare for Making Tax Digital without needing to, or miss a mandatory start date and face a penalty.

Understanding your MTD qualifying income matters. HMRC uses a figure drawn directly from your Self Assessment return — not something you calculate separately and submit later.

This article explains what MTD qualifying income means and which income sources count towards it. It also covers how to locate the right figure on your return, and the scenarios most likely to cause confusion.

By the end, you should be clear on your own MTD qualifying income figure. Understanding that figure is the first step to knowing your MTD position.

Why MTD Qualifying Income Is Not Your Profit

HMRC defines MTD qualifying income as your gross turnover from self-employment and property — before you deduct any expenses. This is the figure that determines your MTD scope, regardless of how much you keep after costs.

The distinction matters enormously for anyone with significant overheads. A self-employed tradesperson with £55,000 in receipts and £20,000 in costs might assume their qualifying income is £35,000.

Under MTD rules, that figure is £55,000 — above the current £50,000 threshold. High-cost businesses can be in scope even when their take-home is well below the limit.

This gross-income rule applies to both sole traders and landlords. For self-employment, qualifying income means your total trading receipts before expenses.

With a property business, it means your gross rental receipts before deducting repairs, mortgage interest, or management costs.

HMRC’s MTD for Income Tax guidance confirms that the threshold is based on gross income, not profit. The official definition is available in HMRC’s MTD for Income Tax guidance on GOV.UK.

Your profit figure plays no part in whether you are in scope. Businesses with identical profits could sit on opposite sides of the threshold because their gross receipts differ.

Which Income Sources Count Towards the MTD Threshold

Two income sources count towards the MTD threshold: self-employment income as a sole trader and property income. If you have both, you combine them.

Any other income you receive does not count towards your qualifying total.

Self-employment income covers all trading receipts from work you carry out as a sole trader. It covers freelance fees, contracting income, and any trading activity reported on your Self Assessment self-employment page.

Property income covers rental receipts from UK property — including residential lets, furnished holiday lets, and commercial lets.

Overseas property income is reported separately and does not count in the current MTD phases.

The following income types do not count towards your MTD qualifying income threshold:

- Your PAYE salary or wages from employment do not affect the calculation.

- Dividends, pensions, savings interest, and capital gains are all excluded.

- Partnership income is excluded, even if you actively work in the business.

- Payments under the Rent a Room scheme and qualifying care receipts do not count.

The salary and side-hustle scenario is worth addressing directly. If you earn a PAYE salary alongside self-employment income, only the self-employment turnover is relevant.

Adding your salary to your freelance receipts could produce a higher figure than HMRC uses. That may create unnecessary concern about being in scope.

Self-employed people with a PAYE job on top need only check their self-employment turnover to know if they need MTD.

The Making Tax Digital overview on taxrebateservices.co.uk covers quarterly reporting and digital records for self-employed people and landlords.

MTD Qualifying Income: How to Find Your Figure

Your MTD qualifying income is not a new calculation. It comes from figures already on your Self Assessment return — the gross income boxes, not profit or loss.

The relevant boxes differ depending on which supplementary pages you complete.

For self-employment using full accounts (SA103F), the qualifying figure is in Box 9 — “Total income from self-employment (turnover).” For simplified accounts (SA103S), use the same box: “Your turnover: the total income from your self-employment.”

The property pages work differently. Your gross rents before expenses are the qualifying figure — Box 20 on the UK property pages (SA105).

If you have both self-employment and property income, you add the two gross figures together. The total is your combined MTD qualifying income.

Take a graphic designer with £42,000 in self-employment receipts and a buy-to-let generating £9,500 in gross rent.

Their combined qualifying income is £51,500 — above the £50,000 April 2026 threshold, even with lower net profit.

One important caveat: these box references reflect the current Self Assessment return format. HMRC occasionally updates form layouts, so confirm current box numbers on GOV.UK before relying on them.

MTD Qualifying Income: Calculating It in More Complex Situations

Four scenarios regularly cause errors in the MTD qualifying income calculation. Each has a specific rule that, once understood, removes the ambiguity.

Jointly owned property.

If you own a rental property jointly with another person, count only your share of the gross rental income. For equal ownership, that means 50% of the gross receipts.

Ceased income sources.

If you ceased a qualifying income source before your MTD start date, that income may still count. Where one of two sources ceases, the remaining source continues to be assessed.

If all your qualifying income sources cease, you fall outside the threshold calculation entirely.

Part-year and new businesses.

HMRC annualises the income of a sole trader business that started or ended part-way through a tax year. A business starting in October with £20,000 in six-month receipts has an annualised threshold figure of £40,000.

For property income started part-way through the year, you apply the same annualisation yourself.

VAT-registered businesses.

If you are VAT-registered, calculate your qualifying income on a VAT-exclusive basis. Use the net receipts — not the gross amount that includes VAT collected on behalf of HMRC.

MTD Qualifying Income Thresholds and Boundary Scenarios

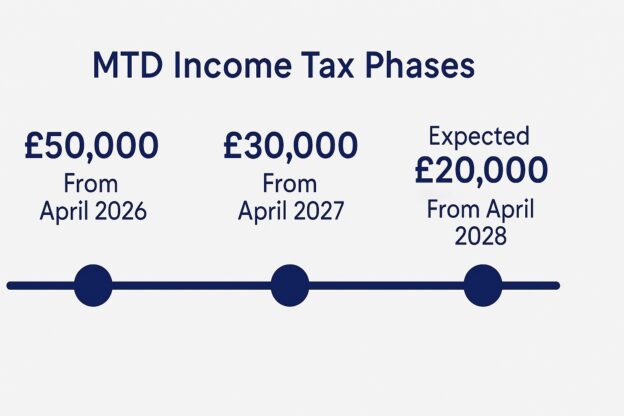

HMRC is rolling out MTD for Income Tax in three phases, each tied to a different income threshold. Which threshold applies to you depends on your MTD qualifying income from a specific past tax year.

For the first phase, starting in April 2026, HMRC uses your 2024/25 Self Assessment return. If your MTD qualifying income for 2024/25 was £50,000 or more, you are in scope from April 2026.

For the second phase, starting in April 2027, the threshold drops to £30,000. HMRC uses your 2025/26 return to make this assessment.

For the third phase, starting in April 2028, the threshold is expected to fall to £20,000. Your 2026/27 return is the relevant one for this phase.

This means your entry into MTD is not based on your current income. It is based on what you declared in a prior tax year.

A change in income since then does not affect which phase you enter. It may, however, matter at future review points.

These threshold figures and dates reflect current HMRC guidance as of 2025/26. The £20,000 threshold for April 2028 has not yet been confirmed in legislation and may change before that phase begins.

If your income drops below the threshold for three consecutive years, you may be eligible to opt out of MTD. Ceasing all qualifying income sources entirely takes you outside MTD altogether.

In Summary

Your MTD qualifying income is a straightforward figure once you know where to look. It is your gross self-employment and property turnover — not your profit or take-home pay.

The figure comes directly from your most recent Self Assessment return. You find it on your self-employment and property pages, not your tax calculation.

The scenarios most likely to cause confusion are joint property ownership, part-year income, and a salary alongside self-employment. Each of these has a defined rule, and none requires a calculation outside your existing return.

Qualifying Income for MTD Key Takeaways

This article covered the following key MTD points:

- MTD qualifying income is your gross self-employment and property turnover before expenses — not your profit, not your take-home pay.

- Only self-employment income and property income count towards the MTD threshold. PAYE salary, dividends, pensions, and partnership income are all excluded.

- Your qualifying income figure comes from your Self Assessment return. Use Box 9 for self-employment (SA103F or SA103S) and Box 20 for property income (SA105).

- Joint property owners count their own share only. HMRC annualises part-year sole trader income, and VAT-registered businesses use VAT-exclusive figures.

- The three MTD threshold phases use these return years and limits: 2024/25 for £50,000 (April 2026); 2025/26 for £30,000 (April 2027); 2026/27 for £20,000 (April 2028, pending confirmation).

- If your MTD qualifying income stays below the threshold for three consecutive years, you may be able to opt out.